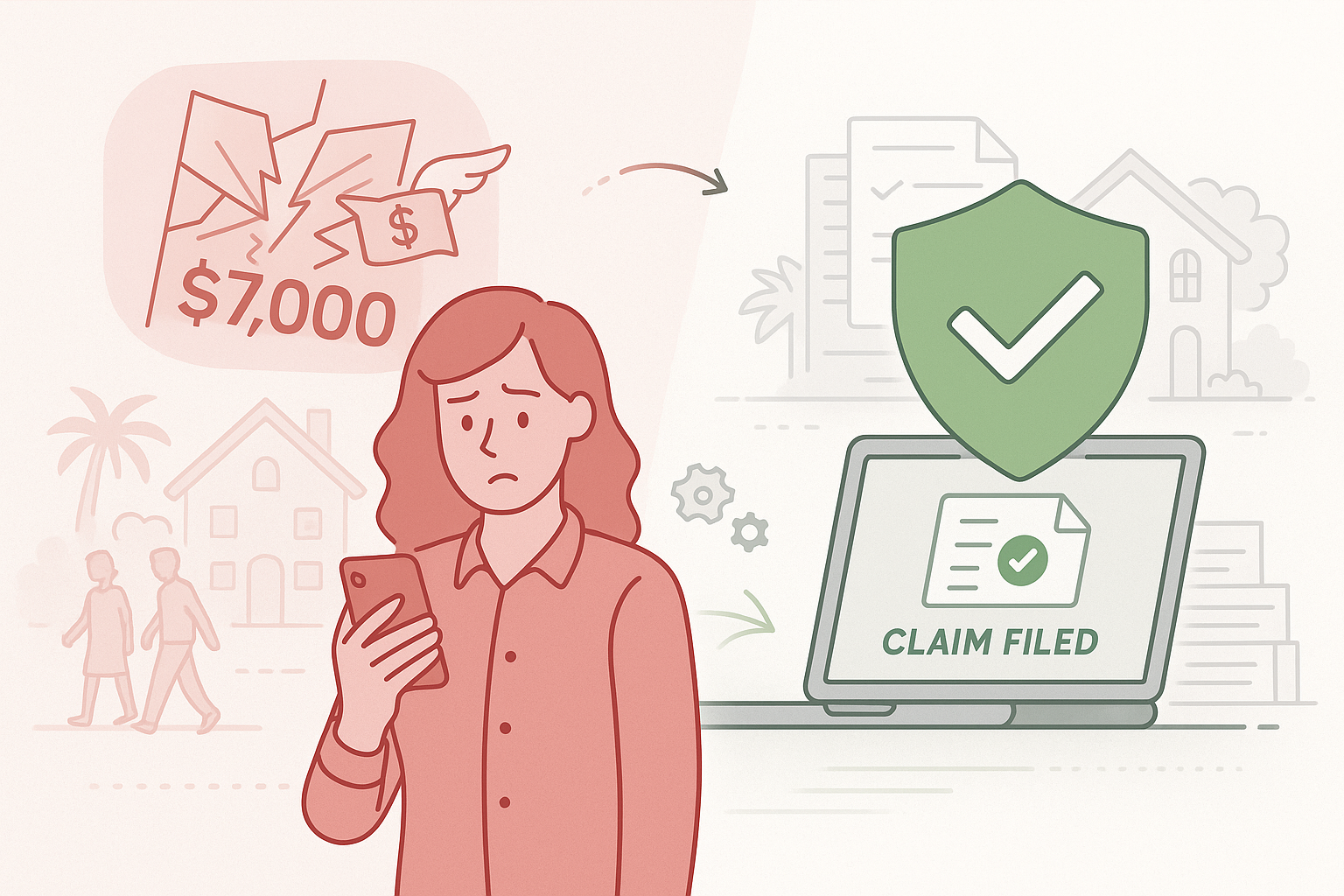

A property manager stares at her phone, waiting for a response that will never come. Two days ago, guests broke $7,000 worth of custom stained glass doors at one of her managed properties. They were “super apologetic and willing to pay” when they checked out. Then she sent the replacement estimate. Now? Complete silence.

This scenario plays out hundreds of times daily across the vacation rental industry. Property owners operate under a simple assumption: if a guest breaks something, they should pay for it. It feels fair. It seems obvious. But this belief in guest accountability might be the most expensive mistake in property management.

This guide reveals why chasing guest accountability fails, what liability risks owners actually face, and how professional operators handle property damage without losing sleep or money.

The Guest Accountability Trap: Why “They Should Pay” Doesn’t Work

Most rental property owners start with residential thinking. Your neighbor breaks your fence? They pay for it. Someone damages your car? Their insurance covers it. But vacation rentals aren’t personal contexts, they’re commercial hospitality businesses where different rules apply.

The guest accountability model collapses when it meets reality. Guests who seemed responsible vanish after seeing repair costs. Platform damage protection comes with 25-day processing delays. Legal action means years of litigation for uncertain recovery.

The Disappearing Act: What Actually Happens After Damage

Property managers report the same sequence every time. Guests acknowledge damage and express willingness to make things right. Everything seems cooperative until actual replacement costs appear. Then communication stops completely.

Platform damage claims take 25 days or more just to start processing. Pursuing lawsuits means upfront attorney fees and multi-year timelines for potentially zero recovery. Meanwhile, your property sits vacant with broken fixtures and mounting lost revenue. The harsh reality? Pursuing guest accountability often costs more than simply filing an insurance claim.

The Liability You’re Not Thinking About

Here’s what keeps experienced property managers awake at night: while owners fixate on their broken doors, they completely miss the lawsuit heading their way. The real risk in property damage incidents isn’t what got broken, it’s who got hurt.

When those stained glass doors shattered, the guests could have suffered severe lacerations requiring emergency care. Glass door injuries typically mean hospital visits, potentially surgery, and medical bills that make $7,000 look trivial.

When Property Damage Becomes Your Liability

One experienced host put it bluntly: “Be glad if they don’t have a hospital bill and sue YOU.” The silence after damage might not be avoidance, it could be preparation for their own legal action against you.

Severe cuts from broken glass often require emergency treatment, stitches, or surgery. Guests can sue property owners for maintaining unsafe conditions or hazardous fixtures. Even winning the lawsuit costs tens of thousands in attorney fees. Liability claims affect your insurance rates and coverage availability for years.

Professional property management means understanding that every damage incident is also a potential liability event. Systems like AdvanceCM help managers document incidents properly and maintain the paper trail that protects you when things go wrong.

Business Insurance vs. Guest Accountability: The Professional Reality

The vacation rental discussion forums show a stark divide. New owners ask, “How do I make the guest pay?” Experienced operators respond differently: “You are a business, and your customer broke a glass door. This is an issue for your insurance, not for them.”

This represents the fundamental shift from amateur hosting to professional property management. Damage isn’t a personal offense, it’s an operational cost.

The Real Cost Comparison

Guest Accountability Path:

- Lawyer fees for demand letter: $500-1,000

- Filing lawsuit: $2,000-5,000 upfront

- Timeline: 2-3 years minimum

- Recovery: Uncertain

- Total: $2,500+ with no guarantee

Business Insurance Path:

- Deductible: $500-2,500

- Processing: 2-4 weeks

- Coverage: Contractual

- Continuity: Immediate

- Total: Deductible only, predictable timeline

One approach treats damage as a personal wrong requiring punishment. The other treats it as a business expense requiring efficient handling. According to the Insurance Information Institute, commercial property insurance specifically covers customer-caused damage as a standard business risk.

The Furnishing Mistake That Makes Everything Worse

Before debating who pays for damages, property managers need to address a more fundamental question: why are there $7,000 custom stained glass doors in a short-term rental at all?

The property manager admitted these doors were a holdover from when the place was the owner’s family home. “If this had started as an Airbnb,” she noted, “that door would not have been there.” This is the conversion trap that catches thousands of new rental operators.

When Personal Property Meets Commercial Reality

Converting a family home into a commercial rental requires ruthless asset evaluation. Sentimental value doesn’t reduce insurance premiums. Every item needs a single question: “Can I afford to replace this multiple times?”

One community member summarized it perfectly: “Play stupid games, win stupid prizes. $7,000 doors on a short-term rental… and you’re renting to total strangers.” High-value, fragile, irreplaceable items don’t belong in spaces occupied by strangers who may be drinking, celebrating, or simply unfamiliar with your property’s quirks.

Making the Mindset Shift: From Homeowner to Business Operator

The vacation rental industry created an entire generation of “accidental hoteliers”—people running hospitality businesses with residential mindsets. Platforms made listing a property so easy that owners never developed the risk management practices that traditional hospitality operations consider fundamental.

This mindset gap explains why owners fixate on guest accountability instead of business insurance. They’re thinking like homeowners rather than business operators.

What Professional Property Management Actually Requires

Professional operations start with accepting commercial realities. Comprehensive insurance is non-negotiable, not platform protection, not guest deposits, but actual commercial property and liability coverage. Assets must match the business model. If you can’t afford to replace something twice, remove it from the property.

The Small Business Administration specifically recommends commercial property insurance for any business operating from a physical location. Vacation rentals aren’t exceptions, they’re textbook examples of why it exists.

Tools That Support Professional Operations

Modern property management platforms handle the operational side of incidents. AdvanceCM’s task management system creates incident response protocols that automatically trigger when damage occurs. Team members know exactly what to document, who to notify, and how to file claims, eliminating the chaos that makes bad situations worse.

This infrastructure doesn’t prevent damage. It ensures that when damage happens, you handle it professionally rather than emotionally. That’s the difference between operators who scale successfully and those who burn out chasing guests for payments that never arrive. Professional tools and competitive pricing make this infrastructure accessible even for small operators.

📱Join the conversation on Reddit, where hosts are sharing their own experiences with damage incidents and insurance claims.

Conclusion

Guest accountability sounds fair. It feels right. And it doesn’t work. The $7,000 stained glass door incident reveals what experienced property managers already know: chasing guests for damage costs more than the damage itself.

The path forward isn’t about finding better ways to hold guests accountable. It’s about accepting that you’re running a business where property damage is a predictable operational cost. That requires commercial insurance, risk-appropriate furnishing, and systems that handle incidents professionally.

Your next steps are straightforward. First, audit your insurance coverage, ensure you have actual commercial property and liability policies, not just platform protection. Second, walk through your properties and identify high-value or fragile items that need removal. Third, implement incident response protocols so your team knows exactly how to handle damage without chaos.

The choice is clear: spend thousands chasing guests who will never pay, or spend hundreds on insurance coverage that professional operators consider standard practice. Which sounds like a business you’d want to run?

FAQs

Q: Isn’t it unfair to let guests damage property without consequences?

A: Life isn’t fair, business is efficient. Professional hospitality operators accept that customer-caused damage is an operational cost, not a personal wrong. Your insurance premium already accounts for this risk. Chasing guests for accountability typically costs more in legal fees, time, and reputation damage than filing a claim.

Q: What if the damage was clearly intentional or malicious?

A: Even with intentional damage, your first call should be to your insurance company, not a lawyer. Commercial policies cover vandalism and malicious acts. Let insurance handle recovery while you focus on getting the property back online. If criminal behavior occurred, file a police report, but that’s separate from damage recovery.

Q: How much does proper commercial insurance cost for vacation rentals?

A: Commercial property insurance for short-term rentals typically costs $1,000-3,000 annually per property, depending on value, location, and coverage limits. That’s $83-250 per month, less than most owners spend chasing one significant damage claim through legal channels.

Q: Can I require higher security deposits to ensure guest accountability?

A: Higher deposits don’t change guest behavior after significant damage occurs. Guests who cause $7,000 in damage will dispute charges regardless of deposit amount. Focus your energy on proper insurance coverage rather than trying to create financial incentives for guests to be more careful.

Q: What should I document immediately after discovering property damage?

A: Take photos from multiple angles showing the damage and surrounding area. Document any guest communications about the incident. Note the date, time, and circumstances of discovery. File your insurance claim within 24-48 hours, delays can complicate coverage. This documentation protects you whether pursuing insurance claims or defending against guest liability claims.

Welcome to Tokeet’s Podcast — your trusted source for insights, trends, and strategies shaping the vacation rental industry. Each episode features expert interviews, data-driven analysis, and practical tips to help property managers grow their businesses, improve guest experiences, and stay ahead in a rapidly evolving market. Whether you’re new to short-term rentals or managing a large portfolio, tune in to stay informed and inspired.

Episode Description:

Static pricing can make a full calendar look healthier than it really is.

In this episode, we break down how vacation rental managers can use demand, booking pace, market context, and owner goals to make clearer rate decisions.

We also cover why dynamic pricing is not about raising rates every night.

It is about knowing when a date needs protection, when a gap needs movement, and when the rate should stay where it is.

You will also hear how pricing decisions affect owner conversations, team workload, and listing performance.

Based on the full blog breakdown on dynamic pricing for vacation rentals.

Key Takeaways:

✅ Fast bookings can still signal underpricing

✅ Slow gaps may need rate, stay-rule, or listing review

✅ Dynamic pricing works best with human oversight

✅Owner trust improves when rate logic is clear

✅ Pricing should be reviewed with full booking context

Related Links:Company: https://www.tokeet.com/Blogs: https://www.tokeet.com/blog/Blog: Dynamic Pricing for Vacation Rentals: Stop Rate Mistakes 👉https://blog.tokeet.com/dynamic-pricing-for-vacation-rentals/

This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit podcast.tokeet.com